What is Self-Employment Tax?

Self-employment tax is the Social Security and Medicare tax paid by freelancers, independent contractors, and small business owners. While W-2 employees have these taxes withheld from their paychecks (and employers pay half), self-employed individuals must pay the entire amount themselves—a whopping 15.3% on top of regular income tax!

Many new freelancers are shocked when they realize they owe not only income tax (10%–37%) but also an additional 15.3% self-employment tax. On $100,000 of self-employment income, that's $15,300 in SE tax PLUS income tax! This guide will show you how to calculate, minimize, and pay this tax correctly.

Breaking Down the 15.3% Self-Employment Tax

The 15.3% self-employment tax consists of two parts:

| Tax Type | Rate | 2026 Wage Base | Purpose |

|---|---|---|---|

| Social Security (OASDI) | 12.4% | First $168,600 | Retirement & disability benefits |

| Medicare (HI) | 2.9% | No limit (all income) | Health insurance age 65+ |

| Additional Medicare Tax | 0.9% | Income over $200K / $250K | High earners surtax |

| Total SE Tax: 15.3% (12.4% + 2.9%) | |||

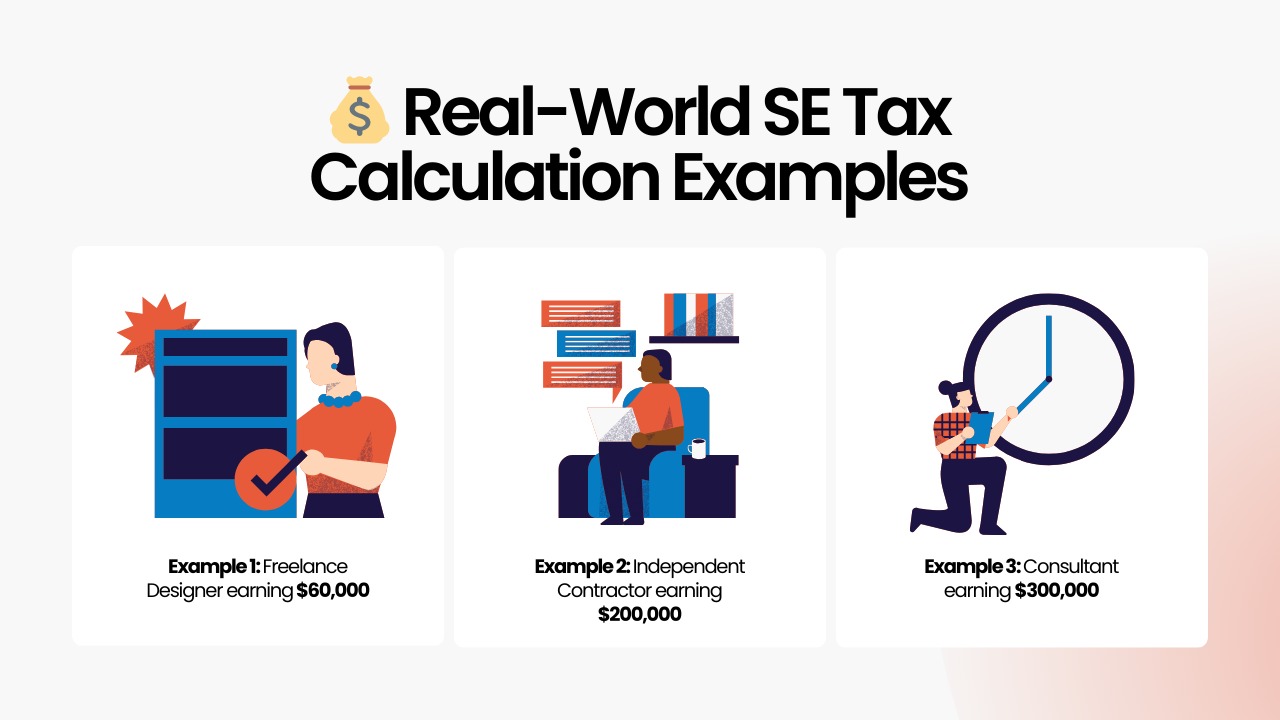

💰 Real-World SE Tax Calculation Examples

📐 Example 1: Freelance Designer earning $60,000

- Net self-employment income: $60,000

- SE tax base (92.35% of income): $55,410

- Social Security: $55,410 × 12.4% = $6,871

- Medicare: $55,410 × 2.9% = $1,607

- Deduction for half: $4,239 (reduces taxable income)

📐 Example 2: Independent Contractor earning $200,000

- Net self-employment income: $200,000

- SE tax base (92.35%): $184,700

- Social Security (capped at $168,600): $168,600 × 12.4% = $20,906

- Medicare (all income): $184,700 × 2.9% = $5,356

- Additional Medicare (over $200K): $0 × 0.9% = $0

- Deduction for half: $13,131

📐 Example 3: Consultant earning $300,000

- Net self-employment income: $300,000

- SE tax base (92.35%): $277,050

- Social Security (capped): $168,600 × 12.4% = $20,906

- Medicare: $277,050 × 2.9% = $8,034

- Additional Medicare (over $200K): $77,050 × 0.9% = $693

- Deduction for half: $14,817

You only pay SE tax on 92.35% of your net income because this mirrors how W-2 employees are treated—they don't pay FICA taxes on the employer's portion (7.65%). The calculation: 100% − (15.3% × 50%) = 92.35%

Schedule C: Reporting Business Income

Self-employed individuals report their business income and expenses on Schedule C (Form 1040). The net profit from Schedule C is subject to both income tax and self-employment tax.

📋 Schedule C Income Sources

- Freelance / consulting income (1099-NEC)

- Cash payments

- Business income

- Other self-employment income

Schedule C Deductions (Ordinary & Necessary Business Expenses):

🏢 Common Business Expenses

- Advertising: Website, business cards, online ads

- Car & truck expenses: Business mileage at $0.67/mile (2026)

- Office expenses: Supplies, postage, software subscriptions

- Legal & professional fees: Accountant, attorney, consultants

- Insurance: Business liability, professional liability

- Travel: Airfare, hotels, meals (50% deductible)

- Utilities: Business phone, internet

- Depreciation: Equipment, computers, furniture

🏠 Home Office Deduction

Two methods to claim home office deduction:

1. Simplified Method:

- $5 per square foot (max 300 sq ft)

- Maximum deduction: $1,500

- No depreciation, easy calculation

2. Regular Method:

- Calculate % of home used for business

- Deduct that % of: mortgage interest, property taxes, insurance, utilities, repairs, depreciation

- More complex but often larger deduction

Requirements:

- Exclusive and regular use for business

- Principal place of business

- Must have profit motive (not hobby)

🚗 Vehicle Expenses

Standard Mileage Rate (2026):

- Business mileage: $0.67 per mile

- Keep mileage log (date, destination, business purpose, miles)

- Cannot use for vehicles used for hire

Actual Expense Method:

- Calculate business use % of vehicle

- Deduct that % of: gas, insurance, repairs, depreciation, lease payments

- Must keep detailed records of all expenses

- Generally better for expensive vehicles

🍽️ Meals & Entertainment

- Business meals: 50% deductible (with clients, prospects)

- Entertainment: Generally NOT deductible (changed in 2018)

- Travel meals: 50% deductible (while traveling for business)

- Office snacks/coffee: 50% deductible

- Company parties: 100% deductible (if for all employees)

Quarterly Estimated Tax Payments

Since self-employed individuals do not receive tax withholding on income, it is necessary to pay estimated taxes quarterly.

If the estimated taxes are not paid, the following penalties apply:

- Underpayment penalty: Interest on the amount owed (currently approximately 8% annually)

- Penalty applies even if a refund is issued upon filing!

- Waiver possible for disaster, casualty, and retirement situations

📅 2026 Quarterly Payment Due Dates:

| Quarter | Income Period | Due Date |

|---|---|---|

| Q1 | Jan 1 – Mar 31 | April 15, 2026 |

| Q2 | Apr 1 – May 31 | June 15, 2026 |

| Q3 | Jun 1 – Aug 31 | September 15, 2026 |

| Q4 | Sep 1 – Dec 31 | January 15, 2027 |

How Much to Pay (Safe Harbor Rules):

✅ Avoid Penalties with Safe Harbor

Pay the LESSER of:

- 90% of current year tax (total income + SE tax), OR

- 100% of prior year tax (110% if AGI over $150K)

- Set aside 25–30% of income: Transfer to a separate savings account

- Pay via IRS Direct Pay: Free, instant confirmation

- Use EFTPS for auto-payments: Schedule all 4 quarters at once

- Adjust as you go: If Q1 was slow, pay less in Q2 (use Form 2210)

- Consider annualized method: If income varies significantly by quarter

Deducting Half of Your SE Tax

Here's the good news: You can deduct 50% of your self-employment tax from your taxable income! This partially offsets the pain of paying both halves of Social Security and Medicare.

💰 SE Tax Deduction Calculation — Example: $80,000 SE Income

- 1

Net self-employment income: $80,000

- 2

Multiply by 92.35%: $73,880 (SE tax base)

- 3

SE tax (15.3%): $11,304

- 4

Deduction (50% of SE tax): $5,652

- 5

Enter on Schedule 1, Line 15

Tax savings from deduction:

- If in 22% bracket: $5,652 × 22% = $1,243 saved

- If in 24% bracket: $5,652 × 24% = $1,356 saved

- Form 1040, Schedule SE: Calculate SE tax

- Form 1040, Schedule 1, Line 15: Deduct 50% of SE tax

- This is "above-the-line" deduction: Reduces AGI (better than itemized)

- No itemizing needed: Can take standard deduction AND this deduction

Self-Employed Health Insurance Deduction

Self-employed individuals can deduct 100% of health insurance premiums for themselves, spouse, and dependents—another "above-the-line" deduction that reduces AGI!

✅ What Qualifies:

- Health insurance premiums (medical, dental, vision)

- Long-term care insurance (limited by age)

- Medicare premiums (if self-employed)

- Premiums for spouse and dependents

📋 Requirements:

- Must show net profit on Schedule C

- Cannot deduct more than net profit

- Cannot claim if eligible for employer plan (yours or spouse's)

- Premiums must be paid with after-tax dollars (not pre-tax through marketplace subsidy)

- Form 1040, Schedule 1, Line 17: Self-employed health insurance deduction

- Do NOT include on Schedule C (reduces income tax but not SE tax)

- This is "above-the-line" deduction (reduces AGI)

Self-Employed Retirement Plans

Self-employed individuals have access to powerful retirement plans with much higher contribution limits than traditional IRAs!

| Plan Type | 2026 Contribution Limit | Deadline | Best For |

|---|---|---|---|

| SEP IRA | Up to 25% of net earnings (max $69,000) | Tax return deadline + extensions | Simple setup, solo business owners |

| Solo 401(k) | $23,000 + 25% of compensation (max $69,000; $76,500 if 50+) | Dec 31 (employee); Tax deadline (employer) | Maximum contributions, high earners |

| SIMPLE IRA | $16,000 ($19,500 if 50+) | Dec 31 for employee; Jan 30 for employer match | Small businesses with employees |

| Traditional IRA | $7,000 ($8,000 if 50+) | April 15 following tax year | Simple, anyone can open |

🏦 SEP IRA Deep Dive — Simplified Employee Pension (SEP) IRA

- Contribution: Up to 25% of net self-employment earnings

- 2026 maximum: $69,000

- Calculation: (Net profit − 1/2 SE tax) × 0.20 = contribution

- Deadline: Tax return deadline including extensions (October 15)

- Setup: Easy, low cost, no annual filing required

💰 Solo 401(k) Deep Dive — Maximum Contributions

Two-part contribution structure:

1. Employee Deferral:

- Up to $23,000 ($30,500 if age 50+)

- Can be Roth or Traditional

- Must be made by December 31

2. Employer Profit-Sharing:

- Up to 25% of compensation

- Can be made until tax deadline + extensions

- SEP IRA: Ideal for simplicity and flexibility — can skip years

- Solo 401(k): Ideal for maximum contributions — can borrow money

- Roth: Ideal for Solo 401(k) to make Roth contributions

- Deadline planning: Employee contributions to 401(k) are due Dec 31

Qualified Business Income (QBI) Deduction: 20% Off!

The QBI deduction (Section 199A) lets self-employed folks deduct up to 20% of qualified business income, which translates into HUGE savings!

💰 QBI Deduction Overview

What it is:

- Deduction up to 20% of qualified business income

- Deduction reduces taxable income, not business income

- "Above the line" deduction for all filers

- Take standard deduction AND QBI deduction

📊 2026 Income Thresholds:

| Filing Status | Full Deduction Under | Phase-Out Range |

|---|---|---|

| Single | $191,950 | $50K phase-out range |

| Married Filing Jointly | $383,900 | $100K phase-out range |

| Limitations apply above thresholds for certain businesses (SSTBs) | ||

These occupations are subject to limitations if income exceeds the threshold:

- Health, law, accounting, actuarial sciences

- Performing arts, consulting, athletics

- Financial / brokerage services

- Investing, trading

- If it is an SSTB and income exceeds the threshold, deduction can be zero

🧮 Ready to Calculate Your SE Taxes?

Use our free federal income tax calculator to estimate your self-employment tax, quarterly payments, and deductions for 2026.

Calculate My SE Tax →