Introduction: Why Tax Deadlines Matter

The consequences of failing to meet tax deadlines include facing penalties and interest from the IRS, besides losing the opportunity to save money through tax planning. This is a detailed tax calendar that includes all the tax deadlines for the year 2026, ranging from estimated tax payments to retirement plan contribution limits.

- Late filing penalty: 5% of the unpaid taxes each month (up to 25%)

- Late payment penalty: 0.5% of the unpaid taxes each month (up to 25%)

- Estimated tax penalty: Interest charged on unpaid taxes (approximately 8%)

- Missed Opportunities: Unable to make contributions to prior year retirement accounts after the deadline

AT A GLANCE

2026 Key Tax Deadlines at a Glance

| Date | Deadline | Who It Affects |

|---|---|---|

| Jan 15, 2026 | Q4 2025 Estimated Tax Payment | Self-employed, investors, contractors |

| Jan 31, 2026 | W-2 and 1099 Distribution | Employers, contractors |

| Mar 17, 2026 | Partnership/S-Corp Returns (2025) | Business owners |

| Apr 15, 2026 | Individual Tax Return & Payment (2025) | All taxpayers |

| Apr 15, 2026 | Q1 2026 Estimated Tax Payment | Self-employed, investors, contractors |

| Apr 15, 2026 | IRA Contribution Deadline (2025) | Retirement savers |

| Jun 15, 2026 | Q2 2026 Estimated Tax Payment | Self-employed, investors, contractors |

| Sep 15, 2026 | Q3 2026 Estimated Tax Payment | Self-employed, investors, contractors |

| Oct 15, 2026 | Extended Return Deadline (2025) | Those who filed extensions |

| Dec 31, 2026 | RMD, HSA, FSA, Charitable Giving | Retirees, savers, donors |

MONTH BY MONTH

MONTH BY MONTH

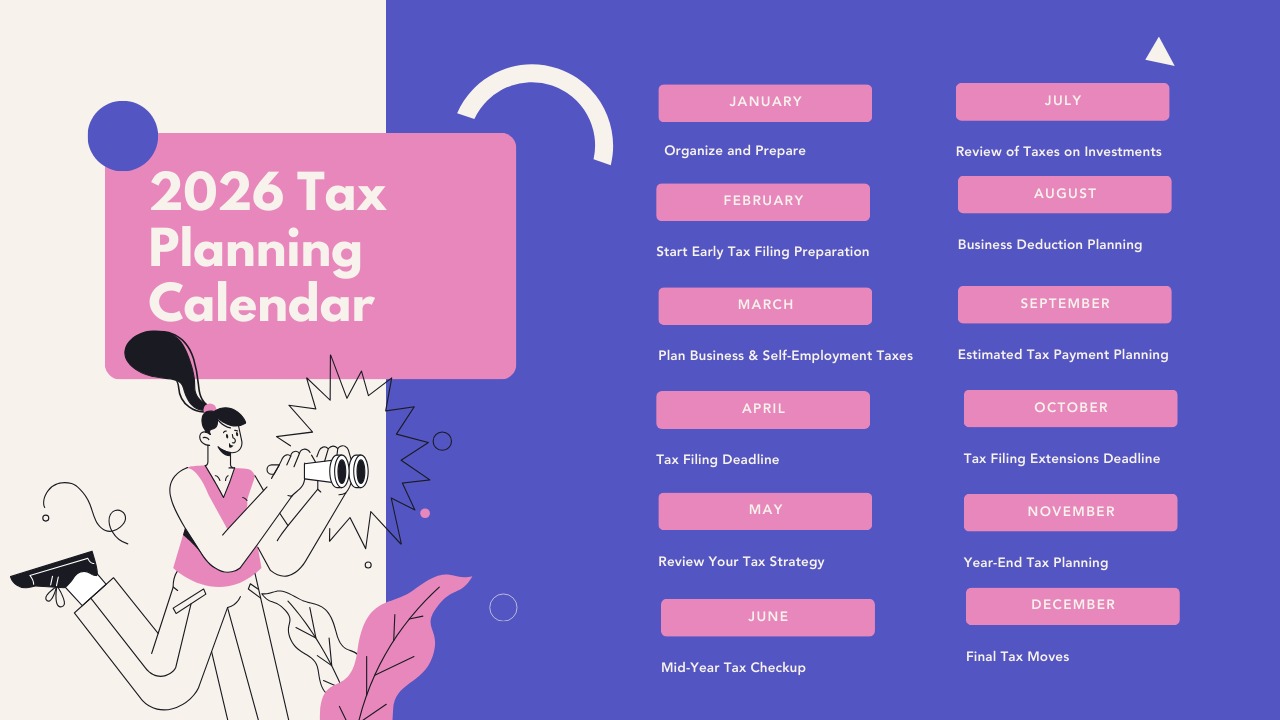

2026 Tax Planning Calendar

🗂️ Organize and Prepare

January is the best time of the year for organizing and preparing your financial records.

- Gather income documents such as W-2, 1099, and investment statements

- Look at last year's tax return for planning purposes

- If you are self-employed, begin tracking expenses

- Check the retirement contribution limit for the year

- Develop a strategy for organizing receipts and other financial records

- Employers send out W-2 forms at the end of January, so keep an eye out for yours

📋 Start Early Tax Filing Preparation

February is a great time to prepare your tax return if you have all your tax documents.

- Check all your tax documents for accuracy

- Check your eligibility for tax credits and tax deductions

- Start preparing your tax return

- Verify your investment income

- Verify medical, education, and charitable contributions

- This will also enable you to receive an early tax refund

💼 Plan Business and Self-Employment Taxes

March is a very important month for people who are self-employed.

- Check your tax liability for the current year

- Organize your business income and expenses

- Check your eligibility for deductions such as home office or equipment

- Consult a tax professional if your finances are complex

- Check if you are eligible for business tax credits

- This will allow you to avoid any surprises later in the year

🚨 Tax Filing Deadline

April is the most important month of the year for taxes.

- File your taxes before the deadline (usually on the 15th)

- File for an extension if you are unable to file before the deadline

- Pay taxes before the deadline to avoid penalties

- Make last-minute IRA contributions for the previous year

- Assess your tax outcome and work on planning for the following year

- Even if you file for an extension, it is important that you make the payment before the deadline

🔍 Review Your Tax Strategy

After the tax season is over, May is the time when you should be reviewing your tax strategy.

- Assess your tax return for planning purposes

- Adjust your withholding if you owed too much or too little

- Update your financial goals for the current year

- Review retirement contributions and savings plans

- This allows you to refine your strategy for the rest of the year

📊 Mid-Year Tax Checkup

By the middle of the year, you should consider the income tax implications.

- Review income tax implications of income and expense to date

- Estimate tax due for the year

- Adjust estimated tax payments as needed

- Explore tax-savings investment opportunities

- Review health savings account contributions

- Having a mid-year tax checkup will help you avoid a large tax surprise

📈 Review Taxes on Investments

Your investment activity will have a large tax implication.

- Review capital gains/losses from investment activity

- Consider tax loss harvesting

- Track dividends from investment activity

- Rebalance investment portfolios for tax purposes

- Planning for investment taxes will reduce the tax implications later

🏢 Business Deduction Planning

Small businesses can greatly benefit from tax planning in August.

- Evaluate equipment purchases and deductions

- Track your mileage and traveling expenses

- Evaluate contractor payments and records

- Plan for potential year-end expenses

- Business spending can greatly reduce taxable income

💰 Estimated Tax Payment Planning

Quarterly estimated tax payments are important for freelancers and business owners.

- Prepare for the third estimated tax payment (due Sep 15)

- Recalculate your expected earnings for the year

- Adjust your withholding if your income changed

- Maintain accurate record-keeping

- Failing to make estimated payments may cause penalties

📁 Tax Filing Extensions Deadline

Taxpayers who requested a filing extension have their final deadline in October.

- File your tax returns before October 15 deadline

- Make the payment if you owe the IRS

- Organize your documents for the current year

- Evaluate your financial progress before start of year-end planning

- After October, focus on the next year's tax season

🎯 Year-End Tax Planning

November is one of the most important months for reducing taxes.

- Acceleration of deductible expenditures

- Postponing income, if possible

- Contributions to retirement plans

- Making charitable contributions

- Harvest capital losses before end of the year

- These strategies will greatly reduce the amount of taxes you have to pay

🏆 Final Tax Moves

December is the last opportunity to make tax-reducing decisions before the end of the year.

- Maximize contributions to retirement plans

- Harvest investment losses if beneficial

- Make charitable contributions before December 31

- Review business expenditures for deductions

- Check the completeness of financial records

- Proper planning in this month will result in huge tax savings

ESTIMATED TAXES

Quarterly Estimated Tax Payments Explained

You should make estimated tax payments quarterly if you are a freelancer, an investor, or have income not subject to withholding.

| Quarter | Income Period | Payment Due Date |

|---|---|---|

| Q1 2026 | January 1 – March 31, 2026 | April 15, 2026 |

| Q2 2026 | April 1 – May 31, 2026 | June 15, 2026 |

| Q3 2026 | June 1 – August 31, 2026 | September 15, 2026 |

| Q4 2026 | September 1 – December 31, 2026 | January 15, 2027 |

How Much to Pay — Safe Harbor Rules (No Penalties):

Pay the LESSER of:

- For Farmers/Fishermen: Only 1 payment due Jan 15 (2/3 of estimated tax)

- For high-income earners: 110% safe harbor if prior year AGI > $150K

- Annualized Income: Can use actual income for each quarter (Form 2210)

- Use IRS Direct Pay for payment (free, instantaneous confirmation)

- Utilize EFTPS for scheduled payments

- Be certain to enter tax year and quarter for payment

- Retain confirmation numbers for record purposes

- Be prepared to change payments throughout the year based on income received

- Annualized method can also be considered for variable income

STATE TAXES

State Specific Tax Deadlines

While most states follow the federal deadlines, there are a few states that have different deadlines:

- Delaware: April 30th

- Iowa: April 30th

- Louisiana: May 15th

- Virginia: May 1st

- Most other states: April 15th

No state income tax return required:

- Alaska

- Florida

- Nevada

- New Hampshire (dividends/interest only)

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

ACTION PLAN

Your 2026 Tax Calendar Action Plan

Set Up These Reminders Now:

- January 15: Q4 2025 Estimated Tax Payment

- April 15: File Taxes + Q1 Estimated Payment + IRA/HSA Contributions

- June 15: Q2 Estimated Tax Payment

- July 1: Mid-Year Tax Checkup

- September 15: Q3 Estimated Tax Payment

- October 15: Extended Return Deadline

- November 1: Start Year-End Tax Planning

- December 15: Final Push for Year-End Tax Planning

- December 31: RMDs, FSAs, Roth Conversions, Charitable Giving

RESOURCES

Related Tax Resources

🧮 Stay on Top of Your Taxes in 2026

Use our free federal tax calculator and self-employment tools to estimate what you owe each quarter — so you're never caught off guard.

Federal Tax Calculator → SE Tax Guide →